Does anyone have experience with flood zone land in FL? It’s obviously common, I’m just not sure how big of a problem it is for buyers. For example, this one has paved access and enough room to build, but flood zone A takes up over 50% of the lot. Planning and zoning don’t seem to think it’s too much of a problem, but the one agent I got in touch with so far didn’t think it was as valuable as I did. I’m running into a good number of these lots and I’m not sure where my numbers should be. Obviously, a survey would help clarify things, but for the most part, I think it’ll tell me what I already know-- You can fit a house on these lots, but I’m not sure if local buyers would still be scared away… Appreciate anyone’s thoughts.

@scottholmes you could call a flood insurance agent to get an idea of how much insurance would be (you can find one through this flood map tool called Obie Risk). The cost of flood insurance is usually the underlying issue that scares people away from flood zone properties. Even if it never floods, the cost of maintaining insurance can be very expensive in some cases (and if they have a lender, flood insurance isn’t optional, their lender requires them to have it). If you find that the cost of insurance isn’t terrible for this kind of flood zone in this area, it could be one way to mitigate the issue if people ask about it.

You could also investigate the cost of building a house that is engineered to withstand floods (either with a berm around it or a house up on stilts). If someone is really concerned about getting flooded, you can let them know what some workarounds are and how much it costs to deal with the issue.

2 Likes

Agree with Seth on the flood insurance issue. Zone A coverage monthly premium killed any hope of rental cash flow and killed a good lake front house prospect on Clear Lake.

Often shore front lots will extend under water up to half the lot or more, especially in areas of tidal influence. Maybe a good thing if you can put in a dock. Valuing such parcels I only consider the ‘high and dry’ part and wholly exclude the Zone A subsurface area.

Be careful as there are fully submerged lots out there that are mostly? worthless. Whole waterfront subdivision blocks in San Francisco come up at the tax sales. They were platted over 100 years ago in anticipation of reclaiming tidal mud flats. That hasn’t happened yet and it aint going to happen today. But they still sell at auction because the price is ‘such a good deal’ when average homes prices are over a million. Bring a snorkel.

@sean-markey @retipsterseth Thanks so much guys-- just so I’m clear, flood insurance is only necessary for houses that would be built on the flood zone portion of the lot, correct? Otherwise you’re just dealing with home warranty insurance, right?

I’m going to reach out to some insurance/flood insurance providers and see what they say.

Based on:

Woody Wetlands: 3.35ac (64.7%), Evergreen Forest: 1.40ac (27.1%), Grassland/Herbaceous: 0.18ac (3.6%), Developed Medium Intensity: 0.16ac (3.1%), Developed Low Intensity: 0.08ac (1.6%)

Crop Cover: Woody Wetlands: 3.63ac (70.1%), Evergreen Forest: 1.11ac (21.4%), Shrubland: 0.20ac (3.9%), Developed/Low Intensity: 0.16ac (3.1%), Developed/Open Space: 0.08ac (1.5%)

I’m guessing there’s room for a house and a yard, but the rest of the property would be in a flood zone…

Thanks again for the feedback.

I have been involved with construction in flood zones. The answer is: yes you can build there, you just need to be above the “design flood elevation.” You can accomplish this by 1) piers 2) earth mounded elevated slab on grade. All of this equals about 2-3x more for a foundation than a traditional non elevated foundation. Easiest thing to do would be advise the buyer that the house would have to be built on the section of the lot that is not in the flood zone. If you want a more certain answer (don’t take my experience as gospel)…contact a local architect and get his opinion on what an approved site plan layout would be. Perhaps pay him to have the site plan approved by the county/city.

1 Like

@scottholmes Again agree with Seth. Usually a lender is the one that is going to require flood insurance. I do not have recent experience on this point. But I would not make general assumptions about what a lender may or may not require. Have seen them do too many dumb things.

Their guideline might be Flood Zone = Flood Insurance, no exception. Check FNMA guidelines as many lenders seem to develop internal guidelines using FNMA requirements as a base starting point. Conform to FNMA guidelines and you usually find a lender that will agree.

1 Like

Thanks @sean-markey

The FNMA guidelines are pretty straightforward–

https://selling-guide.fanniemae.com/Selling-Guide/Quick-Reference-Materials/#Determining.20if.20a.20Property.20Requires.20Flood.20Insurance

In this particular case, flood insurance would be required if any portion of the principal structure or a detached residential structure were to be in the flood zone.

@scottholmes Should be good to go if there is enough high and dry space. Typical with some shore front property that the dry part of the lot is Zone X and the part that extends underwater or below high tide line is Zone A.

@sean-markey Have a signed purchase agreement. Will update whether it works out or blows up in my face. Adventure!

@scottholmes Life gets interesting when and if you get up in the morning. Best of luck with it. Hope you kill it and make a million.

I usually just read, but I must speak up here to potentially protect one of Seth’s people.

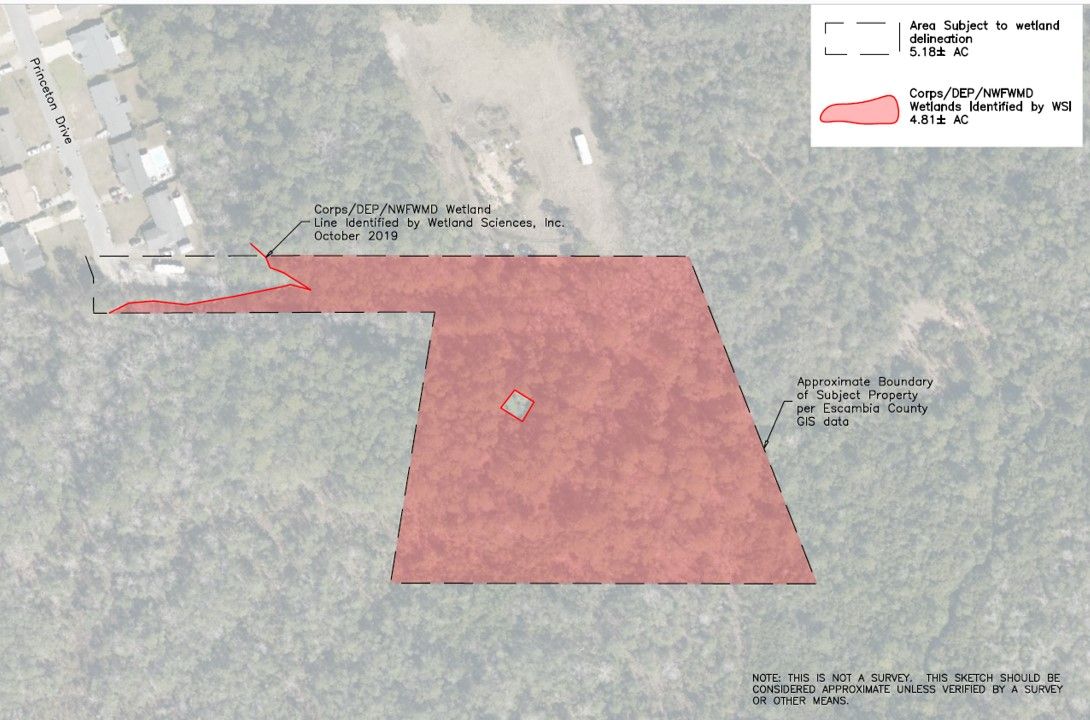

Scott, I strongly recommend that You proceed very carefully with this one.

We bought THIS EXACT PARCEL for $8,000, then had a devil of a time getting it sold for $12,500.

From a Flood Zone perspective, this lot is buildable all day long.

However, the jurisdictional wetlands delineation showed that, while still possible to build, the wetlands situation makes building very much more problematic.

BE CAREFUL. Best of Luck to all.

1 Like

@josh-brooks Whooaa… Putting this on hold. Josh, you available for a quick chat?

Waiting to hear back from Planning and Zoning, but as I go through

How to Identify (and Avoid) Wetlands it appears that even if wetlands were only to cover the back of the property, that’s enough to put a major wrench in building. Multiple government agencies would likely still have to give approval for construction to commence. The soil is also graded a 4, which doesn’t drain well (though it doesn’t seem to have stopped the neighbors from building). Huge thank you to the forum, and of course @Josh-Brooks on my Ready, Fire, Aim approach…

1 Like

Hi Scott, I ran into a similar situation for some lots that were being advertised with soil that didn’t perk (my soil engineer later told me that the soil was the worst type for drainage that he has ever seen). The neighbors in the sub division had traditional septic’s. When I visited the site, I happened to bump into one of the neighbors in the same sub division. I asked how did they get around the soil issue. She kind of laughed at me and just said that the house was built by her father in the 70s, she said, “back then the soil perked, or did it??? ;).” Basically, she didn’t know how they got it approved, but seems to think that her father may have had a really good relationship with the town inspector. So…just because the neighbors got their septic approved, doesn’t mean you will too.

@letsbuildtom Gotcha-- there are basically no new builds in the neighborhood, so it might have been the same approach. Appreciate it.

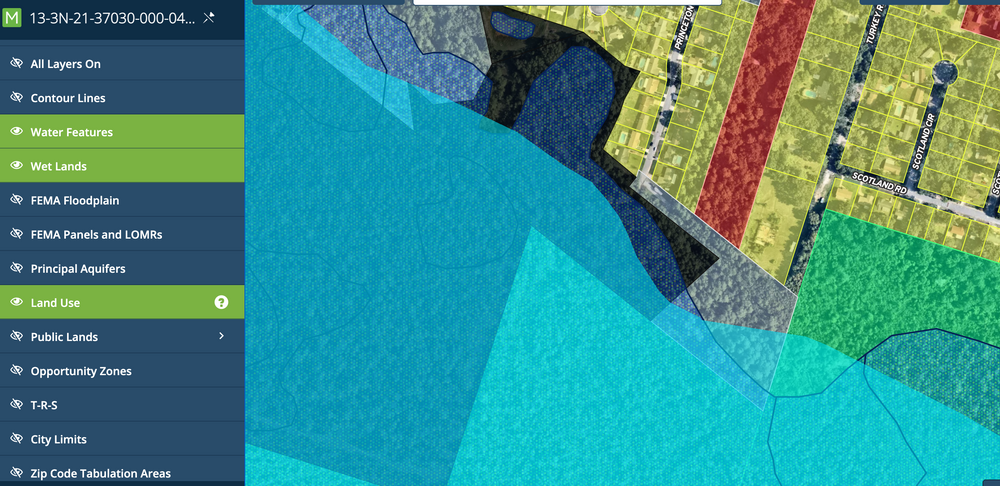

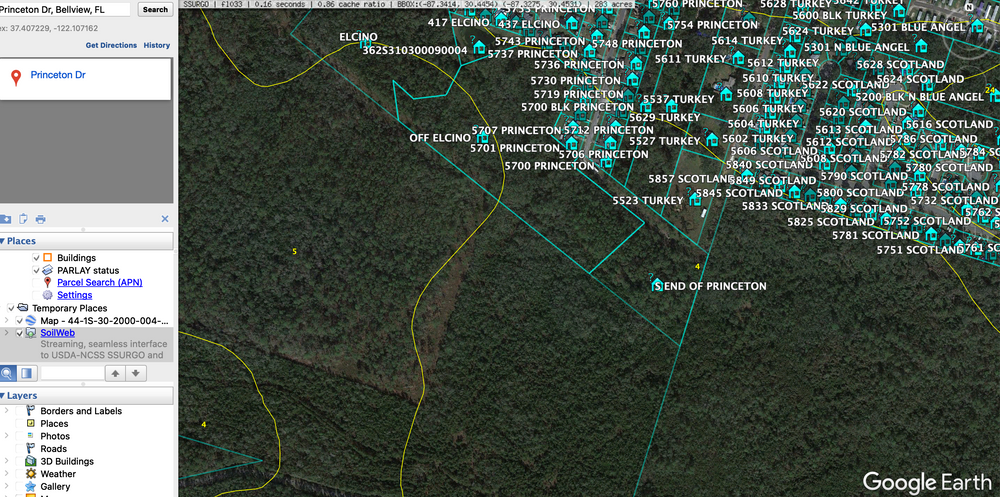

@josh-brooks Just saw your DM-- thanks Josh. To reiterate, I just got bailed out from a 15K mistake by the forum. For entertainment purposes, the Prycd market value for the property was $173,619… I had it coming in closer to 50K (without wetlands…). Josh’s (accurate) Wetlands Delineation map showed that wetlands cover essentially the entire property, while the one I found via the wetlands mapper only had it on the back of the property. Going back and looking at SoilWeb Earth (from Seth’s wetlands video #2), it showed that 85% of the property is “Pickney wetlands - poorly drained.” In the future we’ll be checking the soils report kml on Google Earth as part of due diligence.

2 Likes

Wow! MAJOR props to @Josh-Brooks for catching this and chiming in. I don’t even know what the chances are of that… but I’m really glad the connection was made. Thank you Josh!